Mercury’s Planned Utah Bank Reinforces the State’s Outsized Role in United States Banking

A significant California-based FinTech plans to open a national bank in Utah after receiving "conditional approval" from the U.S. Office of the Comptroller of the Currency, adding yet another proof point to Utah’s rise as a home for nationally scaled banking models.

5 May 2026 — San Francisco and Salt Lake City — Mercury, a San Francisco-based financial technology company, is one step closer to launching a national bank that will be headquartered in Utah.

However, the bigger Utah Money Watch story is not simply that Mercury received "conditional approval" from the Office of the Comptroller of the Currency (OCC) to establish Mercury Bank, N.A.

No, the bigger story is actually that Mercury, a nationally known FinTech platform serving more than 300,000 businesses and individuals, has chosen Utah as the headquarters for its planned full-service national bank.

According to the Mercury news release, the company

- Generates more than $650 million in annualized revenue,

- Has maintained four years of profitability under generally accepted accounting principles (GAAP), and

- Serves one in three startups based in the United States.

The company also said in its news release that 73% of its new customers in 2025 came from outside the tech-startup category.

That makes this more than a FinTech-charter story.

Instead, I believe it's another data point in Utah’s evolution to becoming one of America’s most important banking states.

According to Howard Headlee, President and Chief Executive Officer of the Utah Bankers Association, this planned move by Mercury makes sense on multiple levels.

“Mercury has a highly successful banking model and is well prepared for this moment,” Headlee explained. “We are thrilled that they chose Utah. It validates why Utah has become the 5th largest banking state in America and is the best state to open and operate a bank, especially one as innovative as Mercury.”

Why Utah Matters for Mercury

Clearly, Mercury is not choosing Utah because Utah is a massive end-user market, because it's not, not with a total population barely scratching the 3.5 million mark.

Rather, it's choosing Utah because Utah has become a serious banking-state platform, and that distinction matters.

As noted in the Mercury news release, the company has entered what it described as the “bank organization phase,” during which it will work to satisfy remaining requirements and obtain final authorization from the OCC, along with pending approvals from the Federal Deposit Insurance Corporation (FDIC) and the U.S. Federal Reserve Bank.

During this period, Mercury said customers will continue using the company through its existing partner-bank structure.

And (as noted above), the planned Mercury Bank, N.A. will be headquartered in Utah.

That's the money signal.

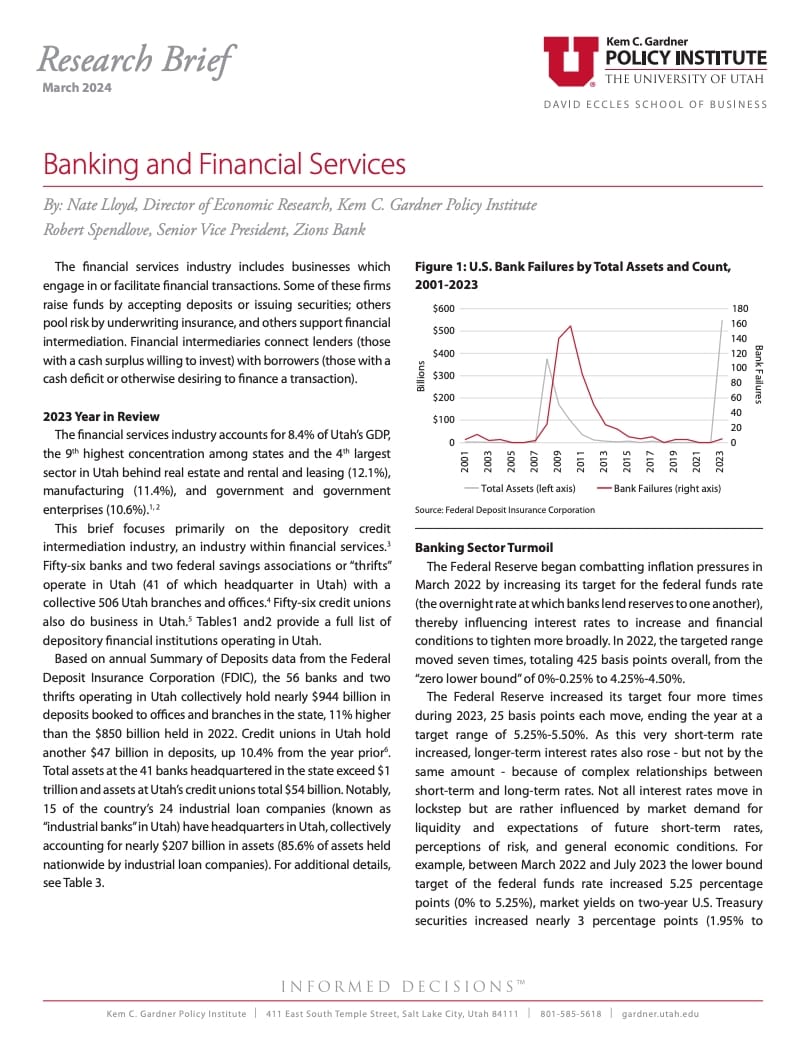

For readers who do not know, Utah already occupies an unusual position in the national banking system.

A 2024 banking and financial-services brief from the Kem C. Gardner Policy Institute reported that 56 banks and two federal savings associations operated in Utah, with 41 headquartered in the state.

The same report said total assets at Utah-headquartered banks exceeded $1 trillion.

To be clear, $1 trillion in assets is not a massive amount on a global scale.

But for Utah? Yeah, it's a pretty solid number.

The same report also noted that 15 of the country’s 24 industrial loan companies (known in Utah as "industrial banks" or ILCs), were headquartered in Utah.

Collectively, these ILCs accounted for nearly $207 billion in assets, or 85.6% of industrial-loan-company assets nationwide.

85.6% of industrial-loan-company assets nationwide are based in Utah.

That does not mean Mercury Bank is being formed as a Utah industrial bank. It is not.

Rather, Mercury is pursuing a national bank charter through the OCC.

But the industrial-bank context matters because it helps explain why Utah has become a preferred home for specialized, technology-enabled, nationally scaled financial institutions.

A Venture-Backed Banking Platform Comes to Utah

There's another layer here too.

Mercury is not a small startup hoping a bank charter will create credibility. Instead, it's already a large, venture-backed financial technology company with significant capital behind it.

In March 2025, Mercury closed a $300 million Series C financing at a $3.5 billion valuation, a round led by Sequoia Capital, with participation from Spark Capital, Marathon, Coatue, CRV, and Andreessen Horowitz.

According to Finovate, the Series C funding brought Mercury’s total investment to $452 million, clearly not shabby.

Such funding history and market valuation perspective is important because it places Mercury's Utah bank announcement inside a larger capital-markets story.

In other words, the company decision is not just regulatory: it's strategic.

Put into a nutshell, a strongly valued, investor-backed FinTech platform is trying to move deeper into direct banking infrastructure, and Utah is the state it has chosen for that next phase.

But there's more.

Mercury: From Partner-Bank Rails to Direct Banking Infrastructure

Today, Mercury emphasizes that it is a FinTech company, not an FDIC-insured bank as its current banking services are provided through partner banks.

The proposed Mercury Bank would, however, change that reality.

According to Mercury, once the bank becomes fully operational, customers are expected to gain access to capabilities they cannot access today, including

- Zelle services built directly into Mercury Bank accounts,

- Expanded lending products for businesses and individuals,

- Deeper payments infrastructure,

- Faster money movement, and

- More direct control over how payments are processed.

That is the deeper financial signal which is all about control of the banking stack.

For years, many financial technology companies have relied on partner banks to provide regulated banking services while the technology company controlled the customer interface. That model helped launch a generation of modern banking products.

But it also left financial technology companies dependent on third-party banking relationships for core infrastructure, compliance, payments, lending authority, and deposit operations.

Now, Mercury is attempting to move closer to the center of the regulated banking system.

And that is where Utah comes into play.

A Familiar Utah Pattern

The Mercury announcement also fits a broader Utah pattern as this is not the first time Utah has appeared at the intersection of

- Banking,

- Financial technology,

- Specialty charters,

- Ownership changes, and

- National financial infrastructure.

For example, here is just a short list for your consideration

💰 Square Financial Services received conditional FDIC approval tied to a Utah industrial-loan-company charter in 2020.

💰 Redemption Holding Company completed its acquisition of Holladay Bank & Trust in 2025, creating Redemption Bank, the only Black-owned bank headquartered in the Mountain West.

💰 And (as reported by Utah Money Watch on 4 December 2025), Provo, Utah-based Green Dot Corp. (NYSE:GDOT) has announce it is being purchased for up to $1.1 billion, taken private, and split into separate banking and financial technology businesses.

Clearly, those stories are not the same as Mercury’s planned launch of a national bank HQ'd in Utah.

But together, they point to the same larger theme:

Utah has become a recurring stage for the national conversation about where banking, financial technology, payments, lending, deposit infrastructure, and regulatory strategy meet.

Utah’s Banking Platform Advantage

Utah’s banking story is often under-appreciated outside financial-services circles, meaning here within the state.

But Utah is not just home to community banks, regional banks, credit unions, and industrial banks.

Instead, it has become a banking-infrastructure jurisdiction, with

- Regulatory experience,

- Institutional memory,

- Specialized legal frameworks, and

- A growing base of financial-services expertise.

That is why the Mercury announcement belongs on Utah Money Watch.

The immediate headline is clearly conditional federal approval, but the larger Utah story is platform validation.

When a nationally scaled FinTech with hundreds of thousands of customers, hundreds of millions of dollars in annualized revenue, roughly $450 million in reported venture and growth funding, and a multibillion-dollar valuation chooses Utah for a planned national bank, it reinforces the same point Headlee made:

Utah has become a serious state for banking formation, banking operation, and banking innovation.

The Poppa P Perspective

To me, the bottom line is this:

Mercury Bank, N.A. is not open yet, and "conditional approval" is obviously not final approval (even though it is a big deal).

Without a doubt, the company still has regulatory work ahead with the OCC, the FDIC, and the Federal Reserve.

But this announcement still matters because banking is not just about where deposits sit.

It is about where financial infrastructure gets built, regulated, governed, and scaled.

For Mercury, the planned bank is about gaining more direct control over its financial platform.

And in the case of Utah, the announcement is another sign that the state’s banking story is no longer just local, regional, or even Intermountain West in scope.

It is national.

And in this case (if everything pans out), it is the story about a financial-technology-native, venture-backed, headed for Utah within a federally regulated construct.

So ... we shall see.

Publisher's Note

This writeup was originally published and distributed to our Subscribers at approximately 10:00am MT on Tuesday, 5 May 2026.

However, if this report/article came to your attention sometime after this date/time and you'd like to change that, then (to become a subscriber), please

1. Click on a "Subscribe" button on any Utah Money Watch webpage (visit www.UtahMoneyWatch.com),

2. Enter in your name in the proper field in the popup window that appears on-screen, and

3. Enter your preferred email address in the proper field too.

That's it. Thanks.

Team Utah Money Watch

Comments ()