Utah’s Deal Market Rebounded to a Record 435 Transactions in 2025, Even as the Disclosed Total Deal Value Dropped to $17.2 Billion on a YoY Basis

The biggest money signal from the MWCN's annual Deal Flow Report (2025) is not a new dollar-value record, because that is not accurate. Rather, it is that Utah’s deal engine kept running in 2025 across a record number of mergers and acquisitions (M&A), public offerings, private placements, private equity rollups, and a broader middle-market capital stack across multiple industry segments — not just the so-called tech-heavy, "Silicon Slopes" ecosystem.

22 May 2026 — SALT LAKE CITY — The 2025 Deal Flow Report was published late yesterday by MountainWest Capital Network, and on the surface, shows what many might perceive as a mixed signal.

On the one hand, equity-related transactions in Utah hit 435 deals in 2025, tying a record set back in 2021.

Conversely, the combined value of said transactions "only" reached $17.2 billion, which (when compared on a Year-over-Year basis to the $39.2 billion and $36.9 billion combo valuations of 2023 and 2024, respectively).

That $17.2 billion figure might be seen as disappointing, perhaps even disheartening ... especially for those who are figurative cheerleaders for the state of Utah and its business community.

But, as I have learned again and again, headlines do NOT always provide a complete picture.

In fact, I have discovered that the best news, information, and data are often found after a bit of digging, prospecting even (if you will).

So when it comes to tracking, analyzing, and reporting on the flow of money in Utah's ecosystem, that's precisely what Utah Money Watch is all about.

That said, announcement-wise, the news from the MWCN is fairly straightforward:

Utah's business ecosystem experienced 435 reported equity-related transactions in 2025, with disclosed deal value reaching $17.2 billion.

That transaction count

- Matched the 435 deals MWCN reported for 2021,

- Exceeded the 423 transactions reported in 2024, and

- Came in well above the 334 transactions reported in 2023.

But the dollar-value side of the scoreboard suggests a very different story.

This is what you find from MWCN’s own data when you look at its reported transaction values (per year) over the past decade, from 2015 through 2024:

- 2015: $9.9 billion,

- 2016: $18.9 billion,

- 2017: $9.2 billion,

- 2018: $13.8 billion,

- 2019: $25.1 billion,

- 2020: $26.4 billion,

- 2021: $31.2 billion,

- 2022: $3.7 billion,

- 2023: $39.2 billion, and

- 2024: $36.9 billion.

Obviously, the totals are all over the map, from a low of $3.7 billion in 2022 to a high of $39.2 billion just one year later, a 10X jump in valuation totals.

Over the 10 year-span, the average (or mean) comes in a $21.4 billion per year.

So, yes, the 2025 amount of $17.2 billion was down sharply from a disclosed value standpoint for both 2023 and 2024, although not that far under the 10-year average.

That's the straight-up truth.

Unfortunately, without context, such information can be misleading.

And this is a case where context matters. A lot.

Specifically, if we're being honest, the 2023 and 2024 comparison years were not normal years.

And they were not; they were outliers.

Or were they?

The Mega-Deal Context

The easiest mistake to make with the combo 2025 number is to compare $17.2 billion against $39.2 billion in 2023 and $36.9 billion in 2024, without explaining what made those earlier totals so large.

The answer is not simply that Utah’s deal market was “better” then and “worse” now.

The answer is that recent years were heavily distorted by unusually large Utah-linked transactions.

Start with 2023.

In March 2023 Silver Lake and CPP Investments announced that they would acquire Provo-linked Qualtrics in a so called "take private" transaction valued at approximately $12.5 billion. The transaction closed on 28 June 2023.

Yes, one deal = $12.5 billion.

One month later, in April 2023, Salt Lake City-based Extra Space Storage announced that it would acquire Life Storage in an all-stock transaction valued at approximately $12.7 billion. That deal closed on 20 July 2023, creating the largest self-storage operator in the United States by store count.

Yes, another deal, this one = $12.7 billion.

Add 'em up and together, those two deals alone represented more than $25 billion of Utah-linked transaction value.

Yup, two deals = $25.2 billion.

That is not normal annual deal flow.

Instead, that is mega-deal distortion.

In other words, if one metaphorically removes those two transactions alone, then that number would have slipped to a still strong $14.0 billion for calendar 2023.

A similar point applies when looking at 2022 through a broader Utah Money Watch lens, even though MWCN’s methodology and timing may not capture every Utah-linked financial transaction.

Case in point, in the 2023 Deal Flow Report, the MWCN reported that there were six equity-transactions in Utah in 2022 of $1.5 billion or greater:

🔹 The $5.2 billion acquisition of Utah-based Vivint SmartHome by NRG Energy;

🔹 The $4.1 billion acquisition of Cloudmed by Utah-based RCM R1;

🔹 The $2.6 billion acquisition of assets of Utah-based Sinclair Oil by HollyFrontier / HF Sinclair;

🔹 The $1.7 billion "SPAC Merger" Initial Public Offering of Utah-based Black Rifle Coffee Company;

🔹 The $1.5 billion Leveraged Buyout (LBO) of Utah-based Entrata by Silver Lake, Dragoneer Investment Group, and HGGC; and

🔹 The $1.5 billion purchase of MountainWest Pipelines Holding Company from Southwest Gas Holdings by Williams (with the understanding that much of the acquired assets are located in Utah).

And yes, simple math shows that these six 2021 transactions had a combined transaction value of $16.6 billion.

Six 2021 transactions = $16.6 billion

Ergo, without them, the figurative value of equity-based transactions in the 2023 Deal Flow Report would have dropped to $20.3 billion, no doubt still a substantial amount, especially for a Utah ecosystem on a per capita basis, one that just hit 3.5 million residents.

But by digging into the past Deal Flow Report data, one realizes that Utah's $17.2 billion in combined equity-transaction value for 2025 is actually quite solid.

The 2025 Scoreboard

The 2025 Deal Flow Report, now in its 31st edition, tracks equity-related, financial transactions connected to Utah, including

✅ Mergers and acquisitions (M&A),

✅ Private placements,

✅ Venture capital,

✅ Private equity,

✅ Angel investments,

✅ Public offerings, and

✅ SPACs (Special Purpose Acquisition Company) transactions.

The basic scoreboard looked like this:

435 reported transactions in 2025, with a combined disclosed value of $17.2 billion.

It was strong, but the value mix was different.

In its 18 May 2026 news release announcing the 2025 Deal Flow Report, the MWCN said the year began slowly, transaction-wise, with uncertainty tied to

▪️ International supply chain disruptions,

▪️ Tariff volatility, and

▪️ Interest-rate instability, before re-accelerating in the second half as

— Engagement letters surged and

— Buyer meetings accelerated.

That sounds right to me as it's obvious the 2025 financial market was not wide open.

In fact, I feel like than corners of the traditional investment community have gone through a multiyear phase of what what has been a right-sizing of valuation expectations, particularly on the money-to-invest side of the table.

To me this has been especially true coming out of the baseline year of COVID-19 and essentially stopped investor money from flowing freely to founders with ideas but no real sales traction.

It's also why I believe that the M&A space has been so hot for the past half-decade.

M&A Led the Way

As usual, M&A carried most of the disclosed dollar value in 2025 in Utah, much as it did throughout the United States and around the globe.

MWCN reported 249 M&A transactions in Utah in 2025 representing roughly $11.75 billion in a combined disclosed value.

Utah's largest disclosed M&A transactions in 2025 were concentrated in substantial, institutional-grade businesses, including

🔺 The $3.05 billion acquisition of Edifecs by Utah-based Cotiviti;

🔺 The $2.10 billion acquisition of Eco Material Technologies by Utah-based CRH;

🔺 The $1.99 billion "take private" acquisition of Utah-based Bridge Investment Group Holdings by Apollo Asset Management;

🔺 The $1.0 billion acquisition of acquisition of Utah-based Sizzling Platter by Bain Capital;

🔺 The $840 million acquisition of Utah-based Bamboo Insurance by CVC Capital Partners;

🔺 The $550 million acquisition of Utah-based SILAC Insurance Company by Hildene Capital Management; and

🔺 The $500 million acquisition of Utah-based RealSource Properties by Utah-based Cottonwood Communities.

When you consider the industry mix from that list above:

⚫️ Healthcare technology,

⚫️ Infrastructure materials,

⚫️ Real estate investment management,

⚫️ Restaurants,

⚫️ Insurance,

⚫️ Multifamily real estate,

It's clear that those are not all Silicon Slopes software deals (although I can guarantee they each have their own unique technology stacks).

But that is part of the point.

Utah’s transaction market is becoming broader than the state’s software-only narrative of the last 20-plus years.

Technology Still Led, But Not Alone

That said, technology still mattered in 2025. A lot.

According to MWCN's 2025 Deal Flow Report, technology represented 39% of Utah’s 2025 deal volume, making it the largest industry category in the Report.

But the more interesting signal may be what happened outside technology.

MWCN also noted that

— Blue-collar services,

— Consumer-service industries,

— Dental services,

— Food & Beverage,

— Healthcare,

— Infrastructure,

— Insurance, and

— Wealth management

each attracted increasing private equity attention.

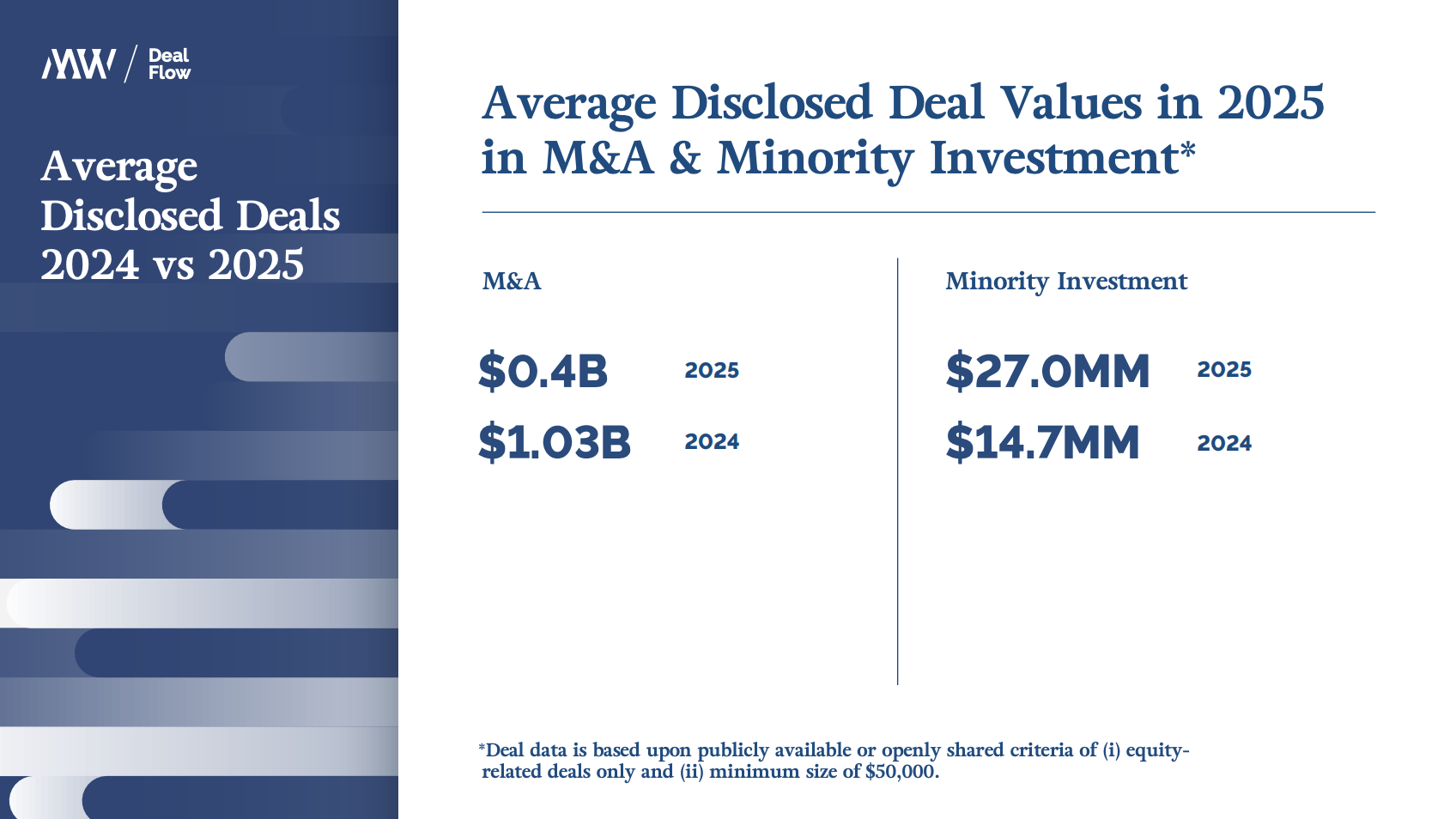

Additionally, there was also a year-over-year shift to

✅ Smaller M&A transactions in 2025 vs. 2024, but

✅ Larger Minority Investments in 2025 vs. 2024 (think family, angel, seed, and Series A investments).

Clearly, those are meaningful shifts.

On the M&A side of the table it suggests Utah’s deal market is no longer only about venture-backed software companies raising growth capital or selling to strategic acquirers.

It's also about rollups, founder exits, cash-flowing service businesses, sponsor-backed platforms, and private equity consolidation.

That does not make as much noise as a $12.7 billion storage merger or a $12.5 billion Take Private deal.

However, it may say more about the underlying health of the market, specifically, the Utah ecosystem.

The Poppa P Perspective

From my perspective, the MWCN's 2025 Deal Flow Report is not a victory-lap document.

Rather, it might be considered a market-reset document.

It shows Utah deal volume returning to record-era levels, while the combined disclosed dollar value approached what should probably be considered a transactional norm, monetarily, especially after accounting for two outlier years.

When looking at MWCN transaction data over the past 10 years,

▪️ Three years came in at over $30 billion (2021, 2023, and 2024)

▪️ Two years came in the $20 billion range (2019 and 2020),

▪️ Two years landed in the teens (2016 and 2018), and

▪️ Three years had single-digit tallys (2015, 2017, and 2022).

And now the 2025 results give us another year in the teens at $17.2 billion.

So does that make 2025 weak? No.

Normal? Honestly, I'm not sure, as it's not apparent to me yet what normal is when it comes to equity-transaction volume in this State of Deseret.

To me the most important aspect about what the 2025 data reveals is both breadth and depth. Hence,

✅ More transactions.

✅ Less mega-deal concentration.

✅ More sector variety.

✅ More private equity interest outside traditional technology.

✅ More evidence that Utah’s capital market is no longer dependent on

▪️ one kind of company, or

▪️ one kind of capital.

That to me is the actual story.

Not “everything is fine” or “Utah set another dollar-value record.”

It did not.

The better read is more disciplined:

Utah produced a high-volume transaction year in 2025 without the same mega-deal stack that made recent years look so large by disclosed value.

That is not only useful information, it tells founders and the investment community that the Utah marketplace is still open, but more selective.

It also communicates that Utah still has deal activity.

Then again, not every year will include two $12 billion-plus transactions.

I believe Utah's Wall Street pipeline is broadening, even as members of the state's ecosystem are reminded that headline numbers alone do not always tell the full story.

Publisher's Note

This writeup was originally published and distributed to our Subscribers at approximately 07:35am MT on Friday, 22 May 2026.

However, if this report/article came to your attention sometime after this date/time and you'd like to change that, then (to become a subscriber), please

1. Click on a "Subscribe" button on any Utah Money Watch webpage (visit www.UtahMoneyWatch.com),

2. Enter in your name in the proper field in the popup window that appears on-screen, and

3. Enter your preferred email address in the proper field too.

That's it. Thanks.

Team Utah Money Watch

Comments ()