Fervo Energy’s $1.89 Billion IPO Turns Utah’s Cape Station Into a Public-Market Geothermal Test Case

Houston-based Fervo Energy soared in its Nasdaq debut yesterday, but the company’s most important proving ground is in Beaver County, Utah where its planned 500-megawatt Cape Station project could help determine whether next-generation geothermal becomes bankable and scalable infrastructure.

14 May 2026 — HOUSTON, SALT LAKE CITY, and MILFORD, Utah — A Houston, Texas-based geothermal company went public yesterday, but the money trail runs straight through rural Utah.

With its initial public offering yesterday, Fervo Energy (NASDAQ:FRVO) priced its stock at $27 per share, selling 70 million shares of Class A common stock in the process and raising $1.89 billion in gross proceeds, before underwriting options.

By the end of trading, Fervo's stock landed at $36.54/share, up 35% from its offering price, giving Fervo a market valuation of nearly $10.1 billion.

But as impressive as that is for a recent Wall Street headline, the Utah story is more specific.

If you don't know, Fervo's flagship development is Cape Station, a multi-phase next-generation geothermal project in Beaver County, approximately 12 miles northeast of Milford.

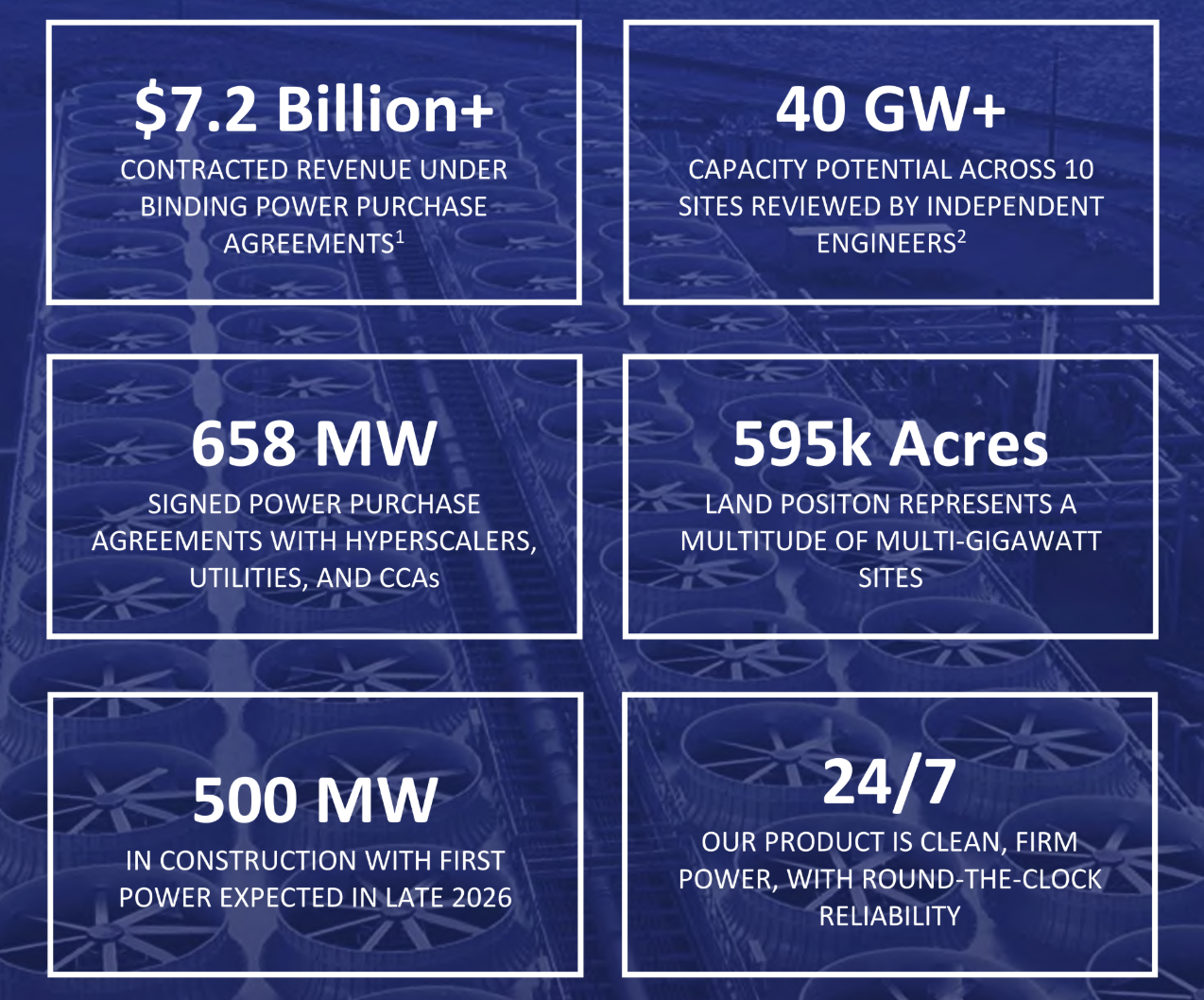

At full-buildout for its planned Phase I and Phase II endeavors, Cape Station is expected to reach 500 megawatts of power generation, with first power targeted by late 2026, approximately 100MW of operating capacity expected by early 2027, and Phase II targeted for 2028.

In other words, the company that just raised nearly $1.9 billion from public investors is not merely telling a geothermal story.

It is asking the market to believe that it can turn underground heat into institutional-scale power infrastructure.

And Fervo's most important proof point is in Utah, which is what makes it a Utah Money Watch story.

Why This Matters

To be clear, this is not merely a clean-energy IPO.

Rather it's a public-market test of whether enhanced geothermal systems can move from promising technology to repeatable infrastructure finance.

Geothermal energy has long been attractive as it can provide around-the-clock underground heat which can be readily transformed into electricity.

Notably, unlike solar and wind, geothermal energy is not dependent on sunshine or wind conditions.

If built at scale, geothermal can operate as what is known in the energy ecosystem as "firm power," power which is increasingly valuable as utilities, data centers, manufacturers, and large power buyers look for cleaner, always-on electricity that is available whenever needed.

That is the market Fervo Energy is trying to capture.

The company says it uses techniques adapted from the oil and gas industry, including horizontal drilling and multi-stage hydraulic fracturing, to produce geothermal energy.

Reuters described Fervo yesterday as part of a broader group of energy developers trying to capitalize on rising demand to power data centers, artificial intelligence, electric vehicles, and domestic manufacturing.

But for Utah, the more important question is narrower:

Can Cape Station become the project that proves next-generation geothermal can be financed, built, contracted, and operated like a real infrastructure asset class ... in Utah?

That is the real test that Fervo is trying to address.

The AI Power Quote That Belongs Here

In a letter included with Fervo Energy's Form S1/A Registration Statement filed with the U.S. Securities and Exchange Commission, Co-Founder and CEO Tim Latimer put the company’s opportunity into one blunt sentence:

“There is no AI revolution without power for data centers.”

That quote explains the market psychology behind the IPO.

Public investors are not simply buying a geothermal company; they are buying a power-demand thesis.

Simply put, the bet is that

🔺 Artificial intelligence,

🔺 Data centers,

🔺 Electrification,

🔺 Manufacturing growth, and

🔺 Grid reliability

will make firm power more valuable.

The Wall Street Journal reported yesterday that Fervo Energy has approximately $7.2 billion in potential contracted revenue backlog tied to power purchase agreements across its portfolio and that it has "... about 600,000 acres of geothermal leases across the Western U.S."

But this is where the Utah angle becomes essential.

If CEO Latimer is correct, then the AI-power story does not run only through data-center campuses, cloud-computing companies, or Wall Street trading desks.

It also runs straight through Beaver County.

That is where Fervo now has to show that its geothermal model can move from investor enthusiasm to operating infrastructure.

The Cape Station Financial Stack

The IPO is the newest layer in a much larger capital stack centered in, around, and through Cape Station.

In June 2025, Fervo Energy announced $206 million in additional financing to advance Cape Station, including

- $100 million in project-level preferred equity from Breakthrough Energy Catalyst,

- A $60 million upsize to an existing corporate term loan facility from Mercuria, and

- $45.6 million in additional non-dilutive bridge debt financing from XRL-ALC, an affiliate of X-Caliber Rural Capital.

At the time, Fervo Energy said Cape Station Phase I would deliver 100MW beginning in 2026, with Phase II bringing an additional 400MW online by 2028, and the full development had permitting approval to expand up to 2 gigawatts.

Then, in December 2025, Fervo Energy announced a $462 million Series E financing to accelerate geothermal development and meet surging demand for clean, firm power. New investors in the round included Google, Mitsui & Co., AllianceBernstein, B Capital and others, along with returning investors including Breakthrough Energy Ventures, CalSTRS, CPP Investments, Devon Energy, Liberty Mutual Investments, Mercuria, and Mitsubishi Heavy Industries.

Then, in March 2026, Fervo Energy announced $421 million in non-recourse debt financing for the first phase of Cape Station. Fervo explained in its release that the financing marked Cape Station’s transition from early-stage and bridge funding to a long-term, non-recourse project capital structure.

Even though the numbers noted above do not represent what the WSJ reported as Fervo's plans to spend $2 billion in Utah alone, that money-flow sequence matters nonetheless as it includes:

✅ Preferred equity,

✅ Corporate debt,

✅ Bridge debt,

✅ Strategic capital,

✅ Series E growth equity,

✅ Non-recourse project financing,

✅ Contracted revenue backlog, and now the transformation into

✅ A fully reporting, publicly traded company.

Simply put, that is the money-flow architecture behind Cape Station.

It's also why Fervo Energy's IPO needed to be reported on and analyzed by a Utah-focused financial media property, even though the company is headquartered in Houston, Texas.

Why Beaver County Matters

Clearly, Cape Station is not in Silicon Slopes or downtown Salt Lake City or even anywhere along the Wasatch Front.

It's some 205 miles south of Salt Lake City in Milford, a region where

🔹 Geology,

🔹 Land,

🔹 Transmission access,

🔹 Permitting,

🔹 Workforce,

🔹 Water, and

🔹 Energy infrastructure

all intersect.

Cape Station's own website says it benefits from confirmed high-temperature resources at depth, proximity to existing transmission infrastructure, geologic data from nearby U.S. Department of Energy research facilities, and adjacency to the Blundell geothermal power plant.

Naturally, that isn't incidental as Utah’s energy future is not being shaped only in boardrooms, legislative hearings, utility planning documents or investor presentations.

It is also being shaped in rural counties where large projects either become real infrastructure or remain ambitious slide-deck promises.

That means major implications for Utah when it comes to

▪️ Rural economic development,

▪️ Tax-base growth,

▪️ Transmission planning,

▪️ Utility procurement,

▪️ Data-center siting, and

▪️ Utah’s broader energy-positioning story,

especially one envisioned and promoted by Governor Spencer Cox with Operation Gigawatt.

Now that Fervo Stock Is Publicly Traded, What Changes?

At a minimum, Fervo Energy walks away from yesterday's IPO with close to $1.88 billion of new money in the bank, and that's important because building out a geothermal company is not cheap.

Additionally, going public also changes the scrutiny.

Dramatically.

As a private company, Fervo could tell a long-term infrastructure story to venture investors, strategic investors, lenders, energy buyers, and project-finance partners without the probing eyes of retail investors.

That is no longer possible.

Instead, everything Fervo does as a public company that a typical retail investor would probably want to know before making a stock purchase or sale decision becomes "material" in nature.

And material information must be disclosed to the public in a timely fashion by firms that have shares available for public purchase.

As a result, Fervo's story now moves into quarterly financial reporting, public-market volatility, analyst coverage, shareholder expectations, and a less patient audience.

That does not make the story weaker; it simply makes the Utah angle stronger.

Fervo Energy's Tim Latimer interview with Ricky Sakai, SVP, New Business Development with Mitsubishi Heavy Industries America in a video titled: "Why Geothermal Energy Is the Sleeping Giant of the Energy Sector." Video downloaded 14 May 2026.

Before the IPO, Cape Station was a major Utah energy development backed by sophisticated private and project-finance capital.

After the IPO, Cape Station is also part of the public-market scorecard for Fervo Energy.

As such, the company now has to prove that enhanced geothermal can be built, financed, contracted, and operated at scale.

And for the next several years, a large part of that proof will come from Utah.

The Poppa P Perspective

From my perspective, the significance of Fervo Energy’s IPO is not simply that a Houston geothermal company had a strong first day of trading, although it did.

That's interesting, though not surprising, but it's also not the deeper Utah story.

The deeper story is that public-market investors just placed a multibillion-dollar valuation on a company whose flagship scale-up project is in Beaver County.

In other words, Cape Station is more than a geothermal development.

In fact, Cape Station is now a public-market test case for whether underground heat can become institutional-scale infrastructure, and that IS a big deal.

For years, the energy ecosystem of Utah has been primarily seen through a lens of petrochemical extraction, and honestly, petrochemicals are obviously still a big deal in the state.

But the success of the Fervo IPO (dramatically supported by the efforts in Beaver County at Cape Station), is another energy sub-sector in the state that significantly contributes to a broadening viewpoint of Utah's energy cluster.

Without a doubt (on both a national and global basis), next generation geothermal endeavors have the potential to create more firm power where none existed before.

And so, Utah is central to the test as Fervo has transitioned into a public company role.

Now, Cape Station becomes part of the public-market evidence trail as well.

And in a kind of "who knew" kind of a way, the entire energy industry is now looking to Beaver County to watch the future of clean, firm power unfold some 12 miles northeast of Milford, Utah.

To me, that's something that is both crazy and awesome at the same time.

Publisher's Note

This writeup was originally published and distributed to our Subscribers at approximately 07:15am MT on Thursday, 14 May 2026.

However, if this report/article came to your attention sometime after this date/time and you'd like to change that, then (to become a subscriber), please

1. Click on a "Subscribe" button on any Utah Money Watch webpage (visit www.UtahMoneyWatch.com),

2. Enter in your name in the proper field in the popup window that appears on-screen, and

3. Enter your preferred email address in the proper field too.

That's it. Thanks.

Team Utah Money Watch

Comments ()