After Publishing a Proprietary Advisor Report in January, Jump closes an $80 million Series B Funding Round Led by Insight Partners

After growing to 27,000 advisors on its platform in just two years, Jump is betting its AI-driven automation and meeting intelligence can deliver measurable ROI.

In fact, its inaugural Financial Advisor Insights Report quantified fear patterns across advisor-client meetings further boosting the firm as it pushes forward with building its “AI operating system” model.

20 February 2026 — Salt Lake City — Just a month after publishing its first data-led market research report, Salt Lake City-based Jump announced yesterday it has closed an $80 million Series B round of funding led by Insight Partners.

To me, the timing of this new funding is important because it serves as a proof point that the AI-empowered "Wealthtech" tools Jump has built for financial advisors and other financial services professionals are gaining traction.

Additionally, the funding announcement (and the underlying impact of the data found in Jump’s inaugural Financial Advisor Insights Report), reinforce the value the firm says it is finding as it accelerates a strategic shift from AI meeting notes into what it calls an AI-native operating system for modern advisory firms.

In addition to Insight Partners, the company’s announcement explains that the Series B round includes participation from new investors F-Prime, Allianz Life Ventures, TIAA Ventures, and Peterson Partners, along with additional investment from existing backers Battery Ventures, Sorenson Capital, Pelion Venture Partners, and Citi Ventures.

Jump said the new financing brings its total capital raised to $105 million, following its $20 million Series A led by Battery Ventures last year.

{AUTHOR'S NOTE: You can review the Utah Money Watch writeup on Jump's Series A funding by visiting "With $20 Million in New Funding, Utah-based Jump Targets a Market Responsible for Over $128 Trillion."}

However, I find it noteworthy that Jump did not disclose valuation, revenue, or any board or governance changes as part of yesterday's announcement.

The “Why Now” is not the Round. It's the Dataset.

Series B rounds are often sold on momentum, and Jump definitely has that.

But what I believe Jump is actually trying to sell is something more durable: a proprietary dataset that claims to quantify what actually drives outcomes inside advisor-client conversations.

In its 2026 Financial Advisor Insights Report (published 07 January 2026), Jump frames conversational intelligence as the missing measurement layer in wealth management, arguing that the industry has historically treated the client conversation as invisible and unmeasured even though trust, planning decisions, and net new assets are often decided in that room.

This is also where the “AI operating system” language becomes clearer.

Jump is not describing or delivering mere note-taking.

Rather, it is describing an intelligence and action layer designed to sit on top of the advisor stack, turning conversations into measurable signals and automated next steps.

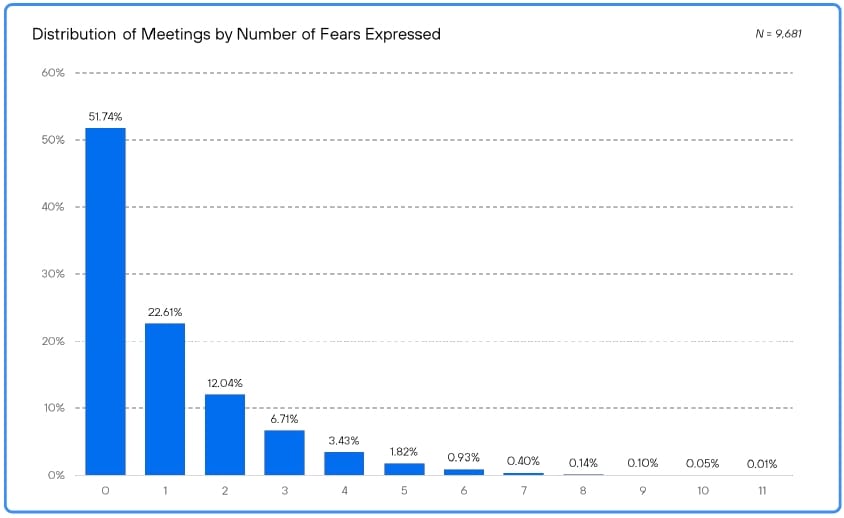

The Jump Report Informs that Nearly Half of Advisor-Client Meetings Included Expressed Client Fears

The Report’s most direct signal is also its most sobering.

Jump says 48.26% of advisor-client meetings included at least one client-stated fear.

And when fear showed up, it is frequently clustered, with 13.59% of meetings containing three or more fears.

The Report further identifies four fears as especially consequential when mapped by both frequency and emotional impact, specifically:

- The inability to pay bills,

- A job or income loss,

- Portfolio losses, and

- Rising taxes.

Read plainly, those topics are less about portfolio construction and more about human stability.

Hence, if Jump is directionally right, the next wave of advisor productivity is not only automation.

It will be the ability to detect emotional risk early, then standardize the firm’s response.

This is why it was able to raise $80 million in new funding.

Its “Predictions for 2026” Puts a Hard Number on Time Savings

A second headline-worthy claim appears in the report’s “Predictions for 2026” section.

Jump states that its users

“... save two to three hours per day, or roughly 300 hours per year, by automating administrative workflows, meeting preparation, follow up and documentation.”

In a business where advisor capacity is one of the scarcest resources, 300 hours per advisor per year is not merely a convenience metric.

Instead, I believe it's a leverage claim, especially for firms trying to grow without adding headcount at the same rate as assets and clients.

Competitive Context: Meeting Notes are Becoming a Feature, Not a Category

The key competitive pressure on Jump is not limited to other AI meeting assistants.

The deeper threat is bundling.

As advisor CRMs and wealth platforms roll AI capture, summaries, and workflow automation into their suites, meeting notes risk becoming table stakes.

And that is why Jump keeps leaning into an operating system posture.

The company is effectively making this claim:

If the market commoditizes note-taking, the winning layer will be the one that turns conversations into measurable firm-wide insights and orchestrated actions.

That's a credible strategy, but it also signals a race within the financial advisory marketplace.

"Follow the Money:" Why I Believe these Four Major Investors are "Leaning in" now with Jump

If you want to understand why this Series B matters, do not start with the $80 million headline.

Instead, start with who wrote the checks, and what each of them is implicitly underwriting.

For example, Insight Partners is a classic growth-stage software investor, and its lead position signals a belief that Jump has crossed from a promising AI tool into a category leader with the potential to become a platform.

In practical terms, that means Insight is not paying for note-taking. Instead, it is paying for distribution, retention, expansion, and a data layer that can become hard for advisory firms to replace once embedded.

Conversely, F-Prime brings a different lens.

F-Prime's history in regulated markets is oriented toward adoption that follows repeatable ROI and enterprise readiness, including compliance, workflow integration, and the ability to deploy at scale without breaking governance.

Then, when examined under a financial microscope, TIAA Ventures and Allianz Life Ventures are the strategic tells.

Wealth management and insurance are ecosystems where trust, compliance, and distribution relationships can decide winners.

When venture arms tied to major financial institutions invest, they are often buying two things at once:

💰 Economic upside, and

💰 A front-row seat to a Wealthtech product that could reshape how advisors operate inside their channels.

I also think that the TIAA and Allianz participation further validates the idea that conversational intelligence can become a durable control point across planning, product adoption, and service workflows.

Taken together, these four names are a market signal that Jump is being valued less as an AI meeting assistant and more as an intelligence and orchestration layer that could sit above the advisor stack.

That is the bet.

If Jump succeeds, it becomes infrastructure.

If it does not, it risks becoming a feature in someone else’s platform.

What's Next

Jump wrote in its news release that the new capital will accelerate product development as it expands from meeting assistance into a broader intelligence and orchestration layer for firms, including Agentic AI capabilities designed to

- Identify opportunities,

- Risks, and

- Next best actions, supported by

- Enterprise-grade controls for large-scale deployments.

At the end of the day, I feel the unanswered question tied to Jump's Series B announcement is straightforward:

Can Jump translate conversational insights into standardized outcomes that large firms can operationalize, measure, and defend in compliance terms?

If yes, the AI operating system language stops being aspirational and becomes a category-defining position.

If not, bundling pressure will keep rising, and differentiation will get harder.

My bet? Jump is on a very good pathway.

{AUTHOR'S NOTE: I interviewed Jump co-founders Parker Ence and Tim Chaves shortly after the company’s Series A announcement last year. Given that experience, this Series B funding announcement reads to me like the same thesis but with a sharper instrument: proprietary meeting-derived insights that quantify fear and workflow friction at scale, then attempt to operationalize that intelligence as a platform. Interesting.}

Publisher's Note

This writeup was originally published and distributed to our Subscribers at approximately 07:40am MT on Friday, 20 February 2026.

However, if this report/article came to your attention sometime after this date/time and you'd like to change that, then (to become a subscriber), please

1. Click on a "Subscribe" button on any Utah Money Watch webpage (visit www.UtahMoneyWatch.com),

2. Enter in your name in the proper field in the popup window that appears on-screen, and

3. Enter your preferred email address in the proper field too.

That's it. Thanks.

Team Utah Money Watch

Comments ()