Centerville's TruGolf Slated to "Go Public" via a $125 Million SPAC-Merger

In spite of the recent collapse of what might be considered the "SPAC Merger Industry," the board and majority shareholders of Centerville, Utah-based TruGolf have opted to "go public" by merging into a "Special Purpose Acquisition Company" in a deal slated to value TruGolf at up to $125 million post-merger.

The SPAC in question is New York City-based Deep Medicine Acquisition Corp. (NASDAQ:DMAQ / NASDAQ:DMAQR), a firm that completed its initial public offering on 29 October 2021, raising $126.5 million gross.

For its part, TruGolf traces its roots back some three decades when it was formed as a subsidiary of Access Software, a firm acquired by Microsoft in 1999 primarily for the success of its Links software title.

Several years later, Microsoft opted to exit the sports software gaming arena and spun-out Access Software to Take-Two Interactive in October 2004 which renamed the company Indie Built.

The transition to Take-Two did not go well, however, and Indie Built was shuttered just 18 months later.

Emerging from the ashes of what had been Access Software was TruGolf, a golf simulation company led by one of the Access co-founders, Chris Jones, an individual with a bit of gamer credibility as the creator behind, and in-game character of, Ted Murphy, what eventually became a six-title, video game series.

And, if you're keeping score, Jones is TruGolf's CEO and Chairman today.

TruGolf is primarily known today for its line of portable commercial, professional, and residential golf simulators, systems with prices that start in the low 10-figures but which are almost universally praised for their industry-leading graphical realism.

A Short SPAC Overview

"Super Lawyer" David Miller and investment banker, David Nussbaum, are credited with crafting the first Special Purpose Acquisition Corporations in the early 1990s, as the two former law school chums joined forces to collaborate with the U.S. Securities and Exchange Commission to establish the parameters for launching such Blank Check companies.

However, in spite of a now 40-year history as financial vehicles for

- Achieving public company status, and

- Extracting value from previously private firms,

SPACs have remained rarely used as instruments for achieving either goal ... until 24 April 2020 when fantasy-sports / sports-betting platform, DraftKings, completed a Blank Check merger.

BTW: DraftKings finished the day with a market cap of over $6 billion.

{NOTE: I am 99.9999% certain that the fact that DraftKings happened to become a public company some five weeks after the beginning of COVID-19 shutdowns in the United States was coincidence and not causal.}

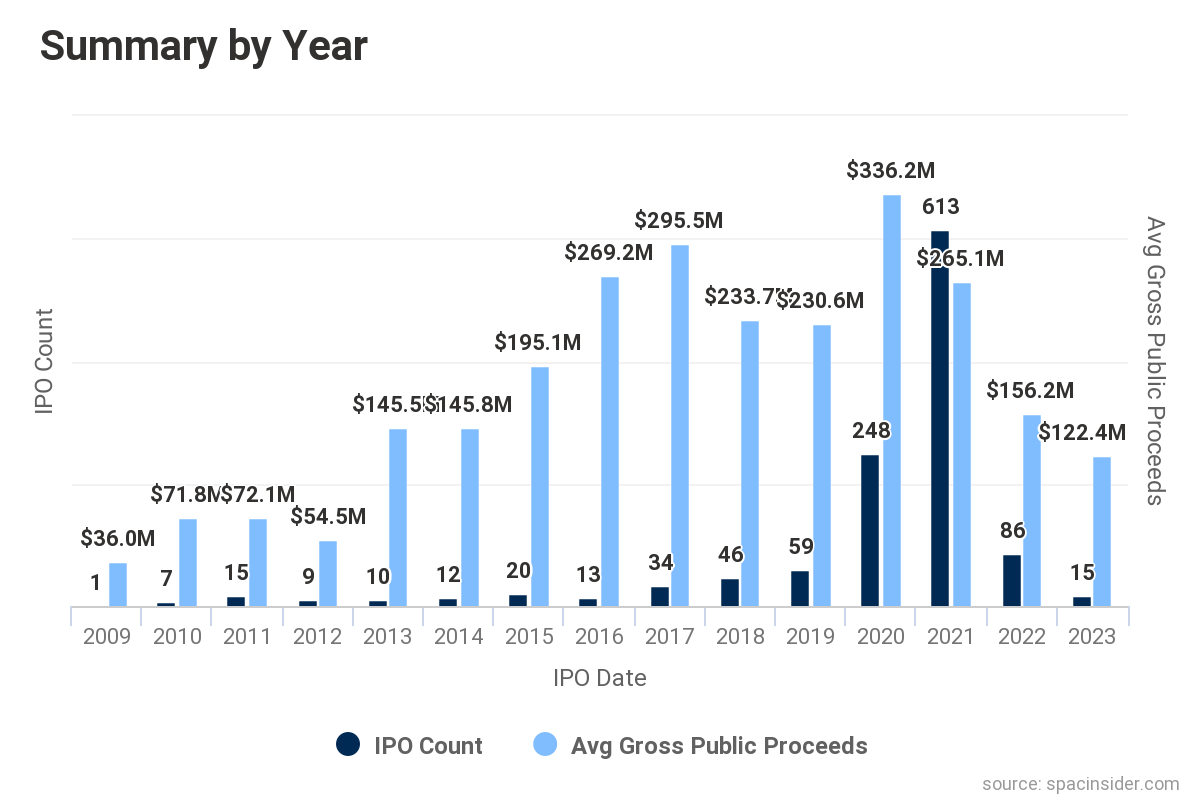

Nevertheless, COVID-19 or not, it appears to this author that the DraftKings SPAC-merger and its subsequent valuation served as the launch point for a land grab in the Blank Check arena, as shown by the SPACinsider.com chart below.

In plain English,

- 2020 saw 248 SPAC IPOs, each raising an average of $336.2 million (for a total of over $83.3 billion raised by Blank Check firms that year);

- 2021 saw 613 SPAC IPOs, each raising an average of $265.1 million (for a total of over $162.5 billion raised by Blank Check firms that year); and even though the numbers tailed off significantly from 2021 to 2022,

- 2022 still saw 86 SPAC IPOs, each raising an average of $122.4 million (for a total of over $10.5 billion raised by Blank Check firms that year).

One of the conditions of creating a SPAC is the legal obligation that a merger with an operating company will occur within a reasonable period of time, typically 18-24 months.

Without achieving such a SPAC merger within the given time frame, or getting shareholders to agree to extend the combination window deadline, these Blank Check companies must de-SPAC, and return the remaining escrowed monies back to their shareholders / investors.

The Pending Deep Medicine / TruGolf SPAC-Merger

As with other SPAC-Mergers, Deep Medicine was also formed as a Blank Check company with the intent to raise monies via an IPO so it could then merge with an existing operating company, providing a financial windfall for both the creators of and investors in Deep Medicine, and (in this case) for the shareholders of TruGolf.

Unfortunately, at this point in the process, there is no information of any analytical use publicly available about TruGolf, making it impossible, today, to provide any insights or commentary as to the proposed valuation of TruGolf post-merger. Obviously, this is disappointing, yet not surprising.

What was a bit surprising to me, however, was discovering that Deep Medicine did begin the process of merging with a different company in mid-2022, a Cayman Islands based firm known as Chijet Motor Company / Chijet Inc.

That merger with Deep Medicine was not consummated and was formally cancelled on 26 September 2022.

Regardless, the more important matter at this point in time is whether or not the two parties, Deep Medicine and TruGolf, will be able to complete the steps required to finish the SPAC-merger by 29 July 2023, as that is the current legal deadline for completing a combination.

If that is not possible, Deep Medicine will need to get its shareholders to authorize the extension of the merger deadline, something I do not foresee as being challenging given that a super majority of the current holders of Deep Medicine's shares are friendly insiders.

But, we shall see.

Comments ()