Utah’s Green Dot Will Be Sold for up to $1.1 Billion in Cash and Stock, Taken Private, and Split in Two by Two Acquiring Firms

If the sale is approved, Green Dot will enter Phase 3 of its 26-year journey by going back to its roots, but within two separate entities: 1) A newly public, $6.3 billion sponsor bank, and 2) A privately held FinTech platform.

And the person behind it all? A serial entrepreneur / investor out of Birmingham, Alabama who sold his firm to Green Dot 11 years ago for "tens of millions of dollars."

4 December 2025 — Provo, Utah-based Green Dot Corp. (NYSE:GDOT) is poised to undergo the most significant transformation in its 26-year history, a transition that, in essence, signifies the beginning of what should be termed the 3rd Phase of its "corporate life."

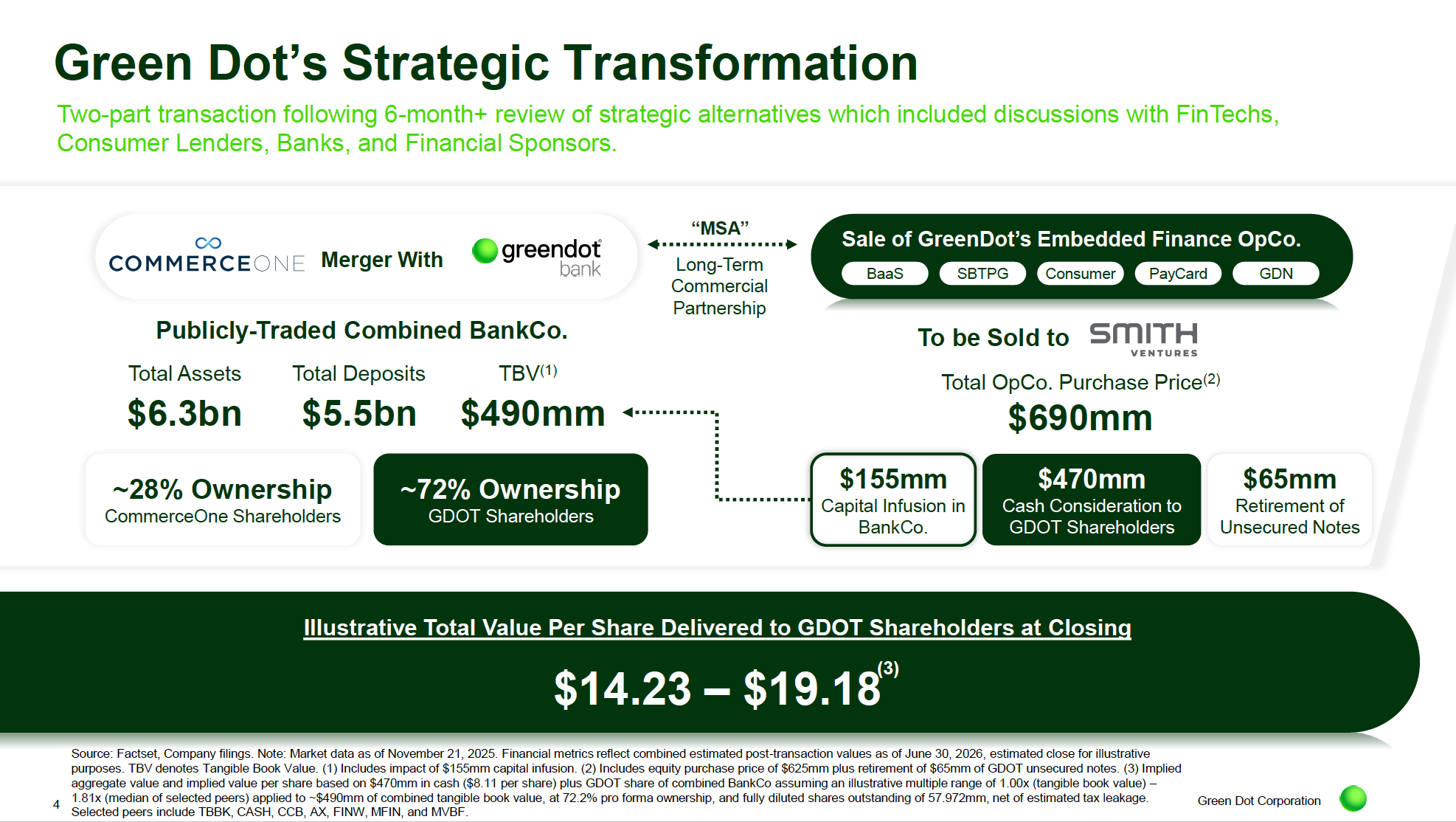

Specifically, the Utah-based FinTech pioneer has announced that it will be sold, taken private, and split into two distinct companies (with one portion becoming part of a new publicly traded firm) — each to be controlled by a different acquiring firm — at a valuation ranging from $825 million to $1.1 billion.

According to the news release announcing the transactions, the two Birmingham, Alabama-based buyers (CommerceOne Financial Corporation and Smith Ventures), are taking separate but interrelated paths in a fairly convoluted yet also somewhat straightforward set of transactions.

To be precise, if/when the transactions are approved (and as noted in the news release, as well as in Slide #4 from Green Dot's investor presentation),

- "CommerceOne will acquire Green Dot Bank and its associated assets and operations," with the banking assets folded into CommerceOne Bank's existing banking operations, with the merged banks

— Having $5.5 billion in deposits and

— $6.3 billion in total assets,

— Adopting the CommerceOne name, and

— Being led by CommerceOne leadership, and

— Becoming a new publicly traded banking company.

Post-acquistion,

- CommerceOne will sell "... Green Dot’s non-bank financial technology business assets and operations ..." to Smith Ventures "... which will continue running (this side of the Green Dot business) as an independent and growth-focused fintech and embedded finance company."

For its part, Smith Ventures will pay $690 million for the FinTech assets of Green Dot, with

- $155 million being paid to CommerceOne,

- $470 million being paid to Green Dot shareholders, and

- $65 million used to "retire" unsecured Green Dot notes.

When the dust settles from the acquisition, breakup, and establishment of the two new companies, Green Dot shareholders will receive

- $8.11 in cash per share of Green Dot, plus

- 0.2215 shares of CommerceOne Bank for each share of Green Dot they held previously.

This means former Green Dot shareholders will collectively own 72% of the new CommerceOne.

Additionally, CommerceOne and Smith Ventures have entered into a separate seven-year agreement that will see the standalone, Smith Ventures-owned FinTech pay ~$30 million in annual fee income to the new CommerceOne for services provided, fees expected to have a Compounded Annual Growth Rate (CAGR) of ~25% or higher.

Under this standalone agreement, CommerceOne

"... will serve as the exclusive bank sponsor for the fintech’s digital banking and embedded finance platform ...."

Pending approvals at the federal and state levels, the parties expect the acquisitions/contracts will close on/before 30 June 2026.

Back to the Future with Green Dot

Although a Utah-headquartered firm since January 1 this year, Wikipedia explains that Green Dot was actually formed in 1999 in Austin, Texas as I-GEN, with its I-GEN debit cards launched a year later and "... marketed toward teenagers and Internet users."

By 2003, these debit cards were available in over 18,000 locations throughout the United States, including "... Rite Aid, CVS Pharmacy, and Pantry Convenience stores."

The following year (2004), I-GEN rebranded as Green Dot, and in 2010 the company went public on the New York Stock Exchange at a valuation of $2 billion.

In 2011, Green Dot became "... a bank holding company under the Bank Holding Company Act ..." when it acquired Provo-based Bonneville Bancorp and its subsidiary, Bonneville Bank.

"This move enabled Green Dot to issue its own prepaid debit cards directly through its banking subsidiary and provide related financial services, enhancing its control over product offerings and customer experience."

Today, prepaid Mastercard and VISA debit cards are offered by Green Dot at more than 100,000 retail establishments in the U.S.

The First Two Phases of the Green Dot Story

To me, the story of Green Dot spans two distinct eras, with a third era/phase about to begin.

Phase 1 (1999–2010) was its rise as a prepaid-card innovator, a consumer-focused FinTech built during the early 2000s wave of reloadable card products and retail distribution.

Phase 2 (2011–2025) began when Green Dot acquired Bonneville Bancorp and instantly became a bank holding company, merging FinTech speed with banking regulation.

At the time, this was one of the earliest examples of a FinTech acquiring a regulated bank, and it was clearly a bold strategic leap.

Unfortunately, this move into banking eventually introduced significant capital and compliance friction.

This second phase has lasted 15 years, and it produced strong revenue growth, major partnerships, and a national footprint.

Unfortunately, it also produced persistent difficulty for Green Dot as highlighted by its inability to convert growing revenue into GAAP-accepted profitability under the weight of regulatory obligations.

At the beginning of January 2025, Green Dot moved its headquarters to Provo, Utah to "... help streamline our corporate and bank operations ..." with its 03 February 2025 news release stating that the firm expected "... little to no change to our growth strategy, focus or day-to-day responsibilities ..."

And (as shown below), when you analyze the numbers Green Dot has been producing of late, the figures are relatively solid.

The Latest Green Dot Financials

For the first nine months of 2025 (ended 30 September 2025), Green Dot finished with

- Revenue of $1.558 billion,

- A net loss $52 million (based on Generally Accepted Accounting Principles), with

- Adjusted earnings before income tax, depreciation and amortization (EBITDA) of $159.6 million.

Those nine-month figures are totally in line with Q3 2025 results of

- $494.8 million in revenue,

- A GAAP net loss of $30.8 million, and

- Adjusted EBITDA of $23.6 million.

To be sure, 2025 has been a solid growth year for Green Dot as third quarter results produced over 21% revenue growth on a Year-over-Year basis vs. 2024 results.

And Green Dot results for the first nine months of 2025 were up ~23% vs 2024 YoY revenue.

The challenge, however, is not the revenue growth.

It's the inability to move to beyond positive EBITDA results into actual profitability that has continued to plague Green Dot, and (in my opinion), led to the (apparently forced) March 2025

- Retirement of Green Dot CEO, George Gresham, as well as

- The disclosure that the company would "... initiate a process to explore potential strategic alternatives."

And roughly six months later, this process has led Green Dot to the apparent beginning of Phase 3 of its corporate life andthe unravelling of its combo Fintech and Bank Holding Company "play," albeit with the pending loss of the Green Dot brand.

Who Wins in these Transactions? Meet Bill Smith: The Alabama Native, Serial Entrepreneur and Investor Pulling the Levers.

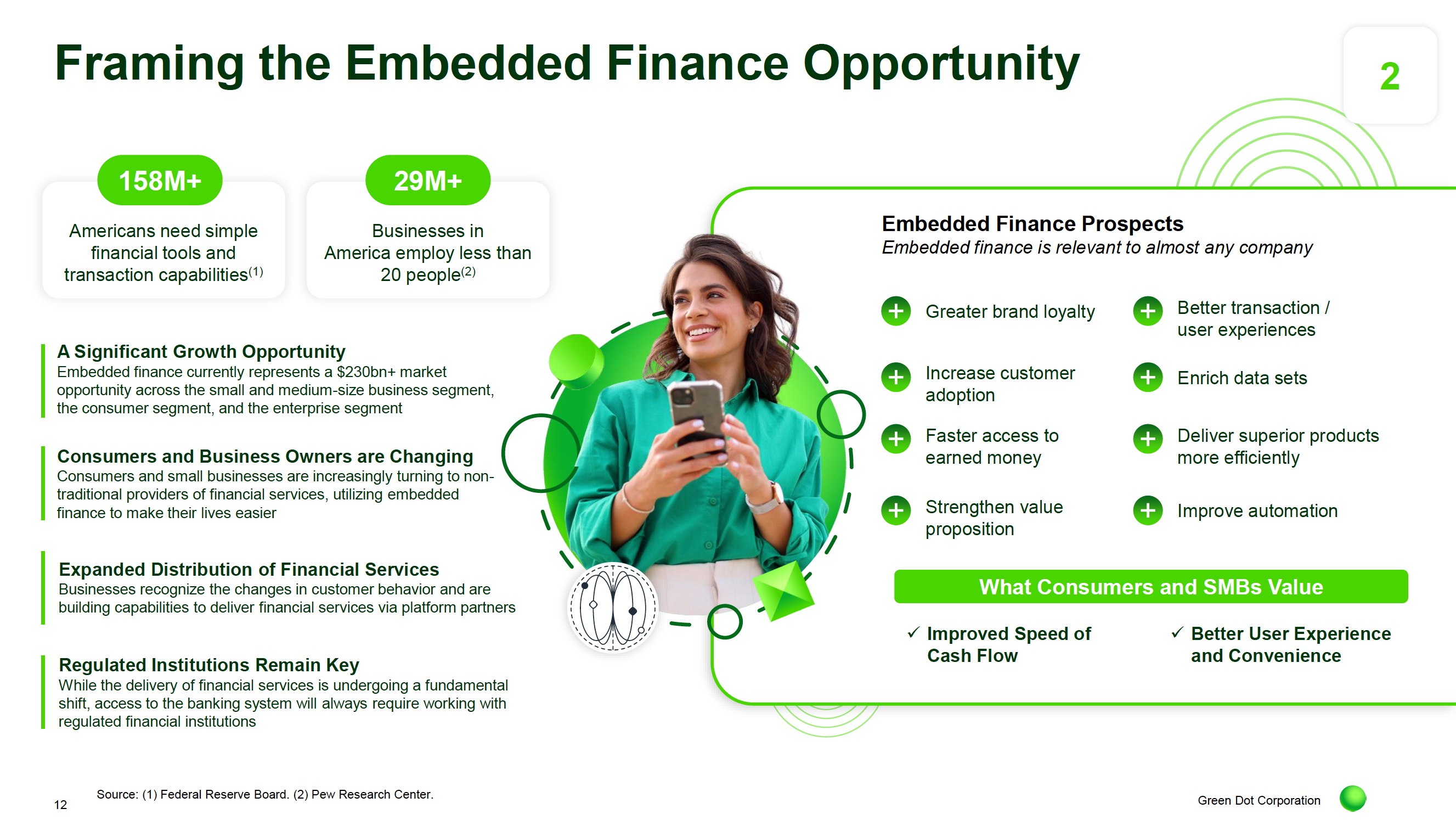

As shown in Slide #12 from the Green Dot investor presentation published late last month (see below), CommerceOne leadership believes that on a post-merger basis, its Total Addressable Market (TAM) will include

- Over 158 million "... Americans (that) need simple financial tools and transaction capabilities...." while

- Over 29 million American small-to-medium-sized businesses "... employ less than 20 people."

In combination, CommerceOne sees the consumer and SMB opportunities as an "Embedded Finance" market worth over $230 billion in annual income.

Although not explained in the acquisition news release, it appears the person behind-the-scenes pulling the various levers in Wizard-of-Oz-like fashion is one Bill Smith.

Smith is the successful Alabama native and Alabama-based serial entrepreneur behind Family Office/Private Equity firm, Smith Ventures.

He also happens to be a co-founder and founding Board Member of Birmingham, Alabama-based CommerceOne Bank.

In other words, it's clear to me that

Smith is the person driving this entire set of Green Dot / CommerceOne / Smith Ventures / FinTech NewCo transactions.

So who is 39-year-old Bill Smith?

An August 2022 feature story on Smith in Forbes provides some interesting background:

- Born and raised in the greater Birmingham area, Smith was "... the son of a Cellular One agent and a medical transcriptionist."

- Before he dropped-out of high school in 2002 at the age of 16, Smith had a side gig selling Nextel phones and pulled-in $5,000/month or more doing so.

- Seven years later (2009), he formed Insight Card Services and sold prepaid and reloadable Visa debit cards.

Hmmmm, what was GreenDot's first product offerings? Yup, prepaid debit cards.

- And, in fact, Smith sold Insight to Green Dot for what Forbes reports was "tens of millions of dollars."

That was 2014, the same year Smith launched Shipt, an online, same-day grocery-delivery service.

Roughly three years later (13 December 2017 to be exact), Target announced it was buying Shipt for $550 million in cash; Smith owned ~50% of Shipt at the time, making him significantly wealthier in the process.

The following year, Smith was a Co-Founder behind the creation and launch of Birmingham-based CommerceOne Bank, where he is also a Founding Board Member.

Yes, the same CommerceOne Bank that plays a central role in this story.

In fact, as Smith explains on his LinkedIn profile:

"CommerceOne holds the distinction of being the first bank charter issued in Alabama and among a very small number in the US since 2009. We completed the state's largest initial bank capital raise in history. The bank primarily serves middle-market businesses and private banking clients. Since its inception, CommerceOne has consistently ranked among the top-performing banks in the US."

And as he wrote on LinkedIn some four months ago:

"I helped found a bank to solve a problem.

"As someone who built several businesses, I knew how crucial it is to have trusted bankers on speed dial.

"That type of service is in short supply, so we built it. CommerceOne Bank was born, and so was our motto: Relentless and responsive."

As it turns out, 2018 was also the year Smith formed Smith Ventures.

In other words, Smith is working all sides of this Green Dot deal, which provides interesting perspectives into the Why's and What-For's driving this announcement and the pending transactions.

So ... What's Next?

Barring some unexpected regulatory wrinkle, I expect this set of multi-party transactions to close sometime before the first of July 2026, as noted in the Green Dot news release.

As a result, Phase 3 of the corporate existence of Green Dot will likely come to fruition sometime in late Q1 2026 or early in Q2 next year, but with such existence continuing forward as two separate entities.

Given that Smith Ventures is based in Birmingham, I see little reason to expect that the FinTech side of the Green Dot business will remain headquartered in Utah, let alone Provo.

Could it? Sure.

But I don't think so.

When would/could this happen?

Clearly, not before the deals are all signed, sealed and delivered.

But after that?

Honestly, it could happen the same day Smith Ventures takes over the Green Dot FinTech operations.

Do I expect Green Dot to move?

Absolutely not, at least not anytime soon.

Why? Because Green Dot is a Utah-chartered bank, and (as my research has taught me), setting-up a banking charter in a new state is not simple or easy.

Rather, it makes more sense to keep Green Dot in Utah, especially because Utah has some of the most favorable state banking laws in the United States.

But the Green Dot brand?

My guess is that the post-merger banking institution will keep both the CommerceOne and Green Dot brands, with

- CommerceOne focused on the business side of banking, and

- Green Dot focused on the consumer side of banking, as a wholly owned subsidiary.

In my opinion, that would be a smart play.

But who knows?

What I do know is this:

Without Bill Smith's involvement, these Green Dot deals would never even been contemplated.

Publisher's Note

This writeup was originally published and distributed to our subscribers at approximately 10:20am MT on Thursday, 04 December 2025.

However, if this article came to your attention sometime after this date/time and you'd like to change that, then (to become a subscriber), please

1. Click on a "Subscribe" button on any Utah Money Watch webpage (visit www.UtahMoneyWatch.com),

2. Enter in your name in the proper field in the popup window that appears on-screen, and

3. Enter your preferred email address in the proper field too.

That's it. Thanks.

Team Utah Money Watch

Comments ()